All enterprises (except sole proprietorships and partnerships), including all organizations that generate income in China, are subject to corporate income tax (CIT).

CIT taxable income is calculated on an accrual basis, meaning that income items are recorded when they are earned and deductions recorded when expenses are incurred. There are two

ways of calculating taxable income: the direct method and the indirect method.

The formula for calculating taxable income under the direct method is as follows:

CIT taxable income = Gross income – Non-taxable income – Tax exempt income – Deductions – Allowable losses carried from previous tax year

Gross income refers to income in currency and non-currency forms received by the enterprise from various sources, including income from the sales of goods; provision of services; transfer

of property; equity investments, such as dividends and profit distribution; as well as interests, rents, and royalties.

Non-taxable income includes fiscal appropriations (e.g., government subsidies to enterprises), governmental administration charges and government funds lawfully collected and brought under relevant laws, as well as other non-taxable income stipulated by the State Council.

Tax-exempt income includes:

- Income from interest on government bonds;

- Dividends, bonuses, and other income from equity investment between qualified resident

enterprises; - Dividends, bonuses, and other income from equity investment received from a resident enterprise by a non-resident enterprise with an establishment or premises in China, with

which the income has an actual connection; and - Income of qualified non-profit organizations.

Example

A company’s annual profit in 2015 is RMB 10 million, RMB 80,000 of which is income from equity investment to a resident enterprise. As this type of income is exempt from CIT, the company can deduct it from its annual profit (i.e., RMB 10 million – RMB 80,000) when determining its 2015 CIT taxable income.

Deductions from gross income include reasonable expenditure incurred in relation to income received by an enterprise, such as costs, expenses, taxes (except CIT and VAT) and losses; charitable donations and gifts within 12 percent of the gross annual profit; reasonable depreciation of fixed assets; amortization of intangible assets; amortization of long-term prepaid expenses; inventory cost; net value of an asset transferred; and other deductions stipulated by laws and regulations.

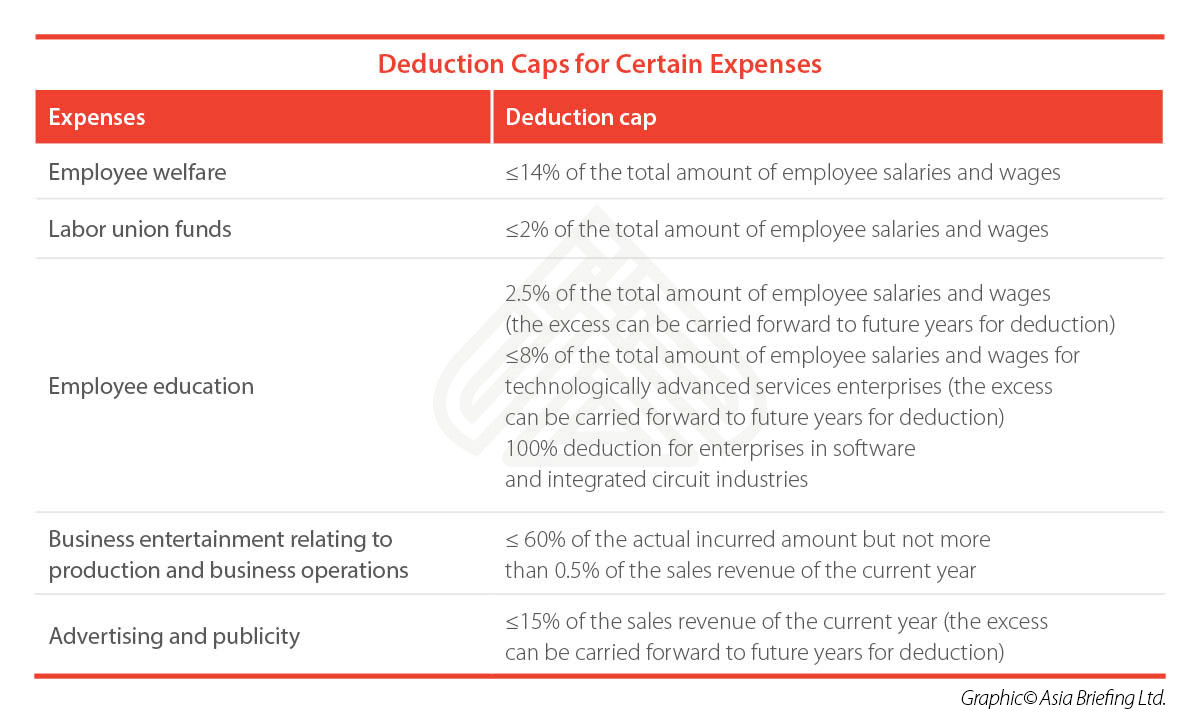

Caps apply when deducting certain expenses from taxable income, such as follows:

A company’s sales revenue in 2015 was RMB 7 million. It incurred RMB 1.5 million in advertising expenses that year.

Maximum amount of deductible advertising expense = RMB 7 million x 15% = RMB 1.05 million

Therefore, RMB 1.05 million of the RMB 1.5 million in advertising expense can be deducted

from the company’s CIT taxable income.

Other permissible deductions include:

- Funds expended for the purpose of environmental protection and ecological recovery in

accordance with applicable laws and administrative regulations; and - Expenses for renting fixed assets to meet production and business operation needs.

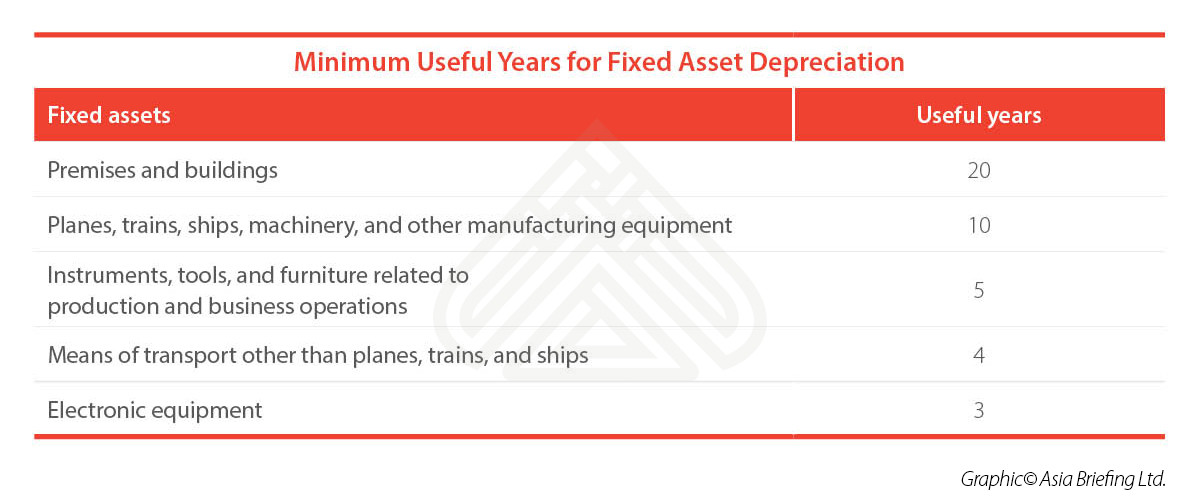

When calculating CIT taxable income, the reasonable depreciation of fixed assets is deductible. Fixed assets refer to the non-currency assets held and used by the enterprises for over 12 months. To determine the depreciation of fixed assets each year, the straight-line method is applied.

The straight-line method takes the purchase or acquisition price of an asset, subtract from it the salvage value, and divide this by the total productive years the asset can be reasonably

expected to benefit the company (i.e. useful life):

Annual depreciation = (Cost – Salvage value) / Minimum useful years

Example

Company A has a piece of manufacturing equipment worth RMB 600,000. The period of minimum useful years is 10 years, and the salvage value is five percent of the original value.

Annual depreciation = RMB 600,000 (1-5%) / 10 = RMB 57,000

Company A can deduct RMB 57,000 from its CIT taxable income.

Non-deductible expenditures include:

- Dividends, bonuses, and other income from equity investment paid to investors;

- Fines for delayed tax payment;

- Penalties, fines, and confiscated property;

- Sponsorship expenditures;

- Non-verified reserves; and

- Other expenditures unrelated to income.

In practice, the indirect method below is more frequently adopted in the annual declaration of CIT:

Taxable income = Gross profit as shown in the accounting book ± Adjustments for tax purpose ± Income/profits to make up for the loss incurred in the previous year

The “adjustments for tax purpose” refers to the discrepancies between applying China’s Accounting Standards for Business Enterprises (ASBEs) and the CIT Law.

Example

Retail company B’s sales revenue in 2015 is RMB 10 million, RMB 1.5 million of which is income from interest on government bonds (which is exempt from CIT). The selling cost is RMB 6 million. The deductible taxes and other relevant expenditures are RMB 1 million. There’s no applicable adjustment for tax purpose and the company also makes profit in the previous year 2014.

The gross profit in the accounting book = RMB 10 million + RMB 1.5 million – RMB 6 million – RMB 1 million= RMB 4.5 million

The taxable income for Company B = RMB 4.5 million – RMB 1.5 million + 0 – 0 = RMB 3 million

References:

- Tax, Accounting and Audit in China 2017, Asia Briefing, https://www.asiabriefing.com/store/book/tax-accounting-and-audit-in-china-2017-9th-edition-7012.html

- How to Calculate Corporate Income Tax in China, Dezan Shira & Associates, https://www.china-briefing.com/news/how-to-calculate-corporate-income-tax-in-china/